Thinking Outside the Box–Supplementing Your Fixed Income

This is an all-ages post, for the most part. You don’t have to be on Social Security or retired in order to have a fixed or limited income. You can be a stay-at-home mom or dad. You can be a college student. You can be someone who is disabled or unable to get enough hours at their current job. In any of these stages, people do lots of things to make their dollar stretch just a little further–cutting corners, coupons, or limiting spending. Others do things like getting part-time jobs or continuing to work through in whatever position of life they are in. This post is about a few things that people in your situation may or may not have thought about doing. These are things geared to put people in a better financial position without breaking the bank. The first topic is geared more for people over 59 1/2, but the rest can apply to anyone.

Making your retirement account work for you

Many of us have accumulated at least some money in a retirement acco unt through our working lives. If you heeded the common advice and didn’t touch the retirement funds at all (or at least very little), that total balance (or balances if you never rolled over old employee accounts) may be quite sizable. However, many of us know to save for retirement, but don’t know exactly what to do once we get there.

unt through our working lives. If you heeded the common advice and didn’t touch the retirement funds at all (or at least very little), that total balance (or balances if you never rolled over old employee accounts) may be quite sizable. However, many of us know to save for retirement, but don’t know exactly what to do once we get there.

In the banking world, I saw people with many different strategies: CDs (bank certificates of deposit), Money Markets, Investments, Annuities, Life Insurance, or just savings. All of these are valid ways of saving and growing to varying degrees, but some of these make more sense in your age group than others. This depends on risk tolerance, of course. In other words, how comfortable are you with the possibility of losing money? Many of us have no idea what “number” to put on that risk tolerance, though! Here’s a great guideline: The rule of 100. Have you ever heard of that? I hadn’t either until I did a little digging. Here’s how it works:

Step 1. Take up an inventory of all of the money that you have anywhere. Don’t forget 401(k)s, Money Markets, CDs, etc. Now, what of that amount is in fixed accounts and what amount is in variable accounts (variable accounts are stocks and bonds and anything that has the word “variable” in the title like variable annuities, variable universal life, etc.). That will give you a clear financial picture.

Step 2. Take your total assets and divide it by the amount of variable assets. Remember this number. Example: if the total amount that you have anywhere is $200,000 and you have $80,000 in variable ($55,000 in stocks and bonds, $20,000 variable universal life, and $5,000 variable annuity), the math you would do is: $80,000 Variable / $200,000 total = 40%. This 40% is the amount of your total money that is at risk. Is this a good number? Well, that depends on step 3, the rule of 100.

Step 3. Take your current age and subtract it from 100. That’s a great guideline of what should at risk (of course, you can go higher or lower depending on how much risk you’re willing to take). This number will get smaller as you get older. So if you’re 60 and number match the ratio above, you’re set (100-60 = 40%). If you’re 70 and match the ratio, maybe it’s time to move money around.

In some cases, it may be a good idea to roll some (but not necessarily all) money into a fixed or indexed annuity. You won’t lose any money there, and you can turn that money into a steady stream of income to supplement your already fixed income. You can see more on this idea here. Every situation is different, so it’s always best to talk to your insurance agent for a plan that will fit your current situation.

Start a Website, no seriously!

Anyone of any age can start a website. You don’t have to be an expert or even know anything about websites to start. There are several programs out there that will help you get a website started for free and give you training on getting your site up and running. You can make a site centered around any topic you like–whatever your passion is. Do you love your dogs? Start a site talking about that. Like music? Start a site related to that. Travel a lot? Start a site where you post pictures of your travels and talk about your experiences. You can actually make a website talking about what you learned while making your website! The possibilities are endless.

What does this have to do with supplementing your income? That’s what’s so cool! Basically, as you get visitors to your site, search engine sites (maybe what you used to find this site) will start to notice your site more, and then you can get more visitors. Visitors then can click on affiliate links on your site (all free) and you get small commissions on those. You may see a link to the right labeled “further reading.” I use stores and links such as these not only to be helpful but also to help pay for some of the things I’m doing online.

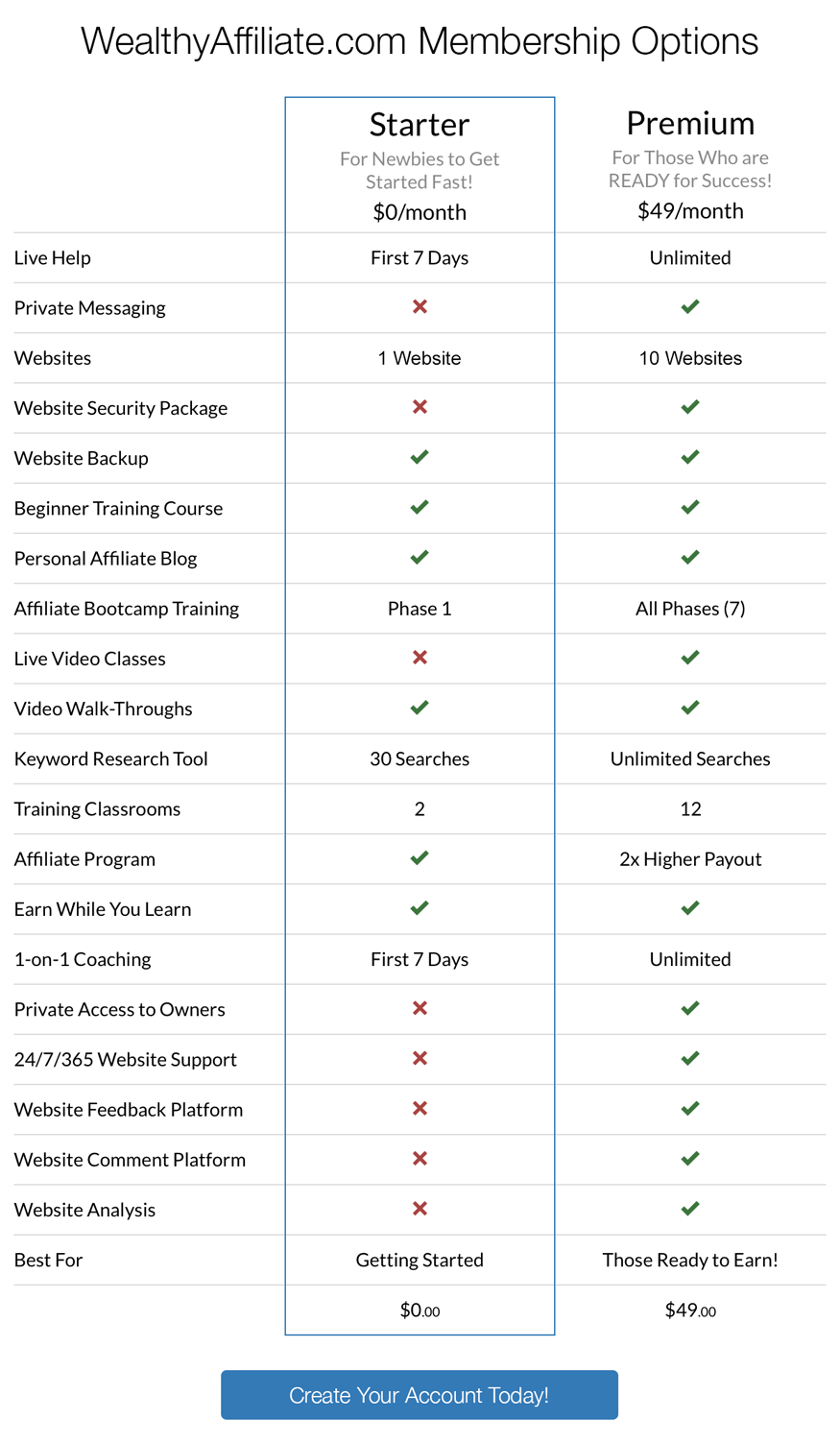

There are a few places that come recommended that will get you going and give you some instruction. My first choice is Wealthy Affiliate. The name may sound “scammish” or a get-rich-quick scheme, but it really isn’t. It is an instructional community that is filled with people who are eager to help you. If you want to know how to do something on your site, you can ask anyone in the community. There are even video instructions on how to create pages, posts, and even make a privacy policy that will pass all standards. The best part is: You don’t have to know anything about computers at all.

There are two “plans” with Wealthy Affiliate. One is free (Starter), and one is $47 per month (Premium). The main differences are really the type of domain names that are supported (mainly important to google, but not for what you put on the site) and how much training, support, and site utilities you get. As you get more into the program, you can change to the paid subscription if you so desire. Here is the breakdown.

It’s worth a shot. If you don’t like it, you’re not out any money, and there are no hidden fees. If you’re able, though, I do suggest the premium membership. All new accounts start with 7 days of premium membership so you can see all the features. There is a link to a free siterubix website on the right column of this page, too, if you’re more interested in just having a free site.

Get on the ground floor of something new

Sites like Facebook started with a handful of people (rumor has it that 5 were called to a meeting and only two showed up. Look at them now!). There are things popping out all over the place on the internet. To some, doing anything on the internet can be intimidating, but don’t worry about that. The thing to know is that there are lots of opportunities out there on the internet for making some extra money without working a typical job. Here’s one that is up and coming.

First, think about the people who invested in Apple when it first founded in 1976. At its inception, the goal was to develop and sell computers. However, now, it’s a multinational company selling phones, mp3 players, music, TV products, etc. Facebook was started in 2006 by 3 people. Now, it is also attached to just about everything we look at! Who’s to say that another company will not grow the same way those have? Take a look at this one:

![]()

IGrowit is another one of those companies, I think. Now, granted, there are a lot of scams out there to look out for, too. This is pretty legit, though, from all that I can see. It is still in its beginning stages, and also is free to get started. This is going to take the popular giant of social media and really capitalize on it. The potential of this company is immense, and I hope those who are looking for something jump in on opportunities like this soon.

As far as cost goes, it is similar to Wealthy Affiliate. But, keep in mind that these are two completely different ways of doing internet marketing. You can actually do some in both if you wanted, or choose one. They are not in competition with one another. With IGrowit, can do most everything on the free (affiliate) account, but the paid (associate) account gets you more perks, instructions, and certifications (more details to follow). The best thing to do is watch this video and get back with me for more information. Be sure to fill out the form to get started. If you would rather see a website explanation, you can go here and read about it.

Combine your passions. What are yours?

Nothing says that you have to pick one thing. If computers aren’t your thing and will never be your thing, these ideas may not seem valid to you. But think about this: Where are you reading this now? There is a very large chance that you are either viewing it on a computer, a tablet, or a phone (or some other type of smart device). There is future in it, for sure, and it’s not too late to get in on it. I would love to hear from you about what things you are doing to supplement your income. Can it be duplicated so that others can do the same thing? Please leave comments below and let me know what you think!

https://simpleseniorhealth.com/thinking-outside-the-box-supplementing-your-fixed-incomehttps://simpleseniorhealth.com/wp-content/uploads/2015/06/Burberry_wallet-768x1024.jpghttps://simpleseniorhealth.com/wp-content/uploads/2015/06/Burberry_wallet-150x150.jpgGeneralIncome OpportunitiesThis is an all-ages post, for the most part. You don't have to be on Social Security or retired in order to have a fixed or limited income. You can be a stay-at-home mom or dad. You can be a college student. You can be someone who is disabled...Raphael raphaelstarr@gmail.comAdministratorRaphael resides north of Indianapolis, Indiana. He is an independent insurance agent. He is also the worship leader at his church, a husband, and step-father of one awesome 15-year-old girl. You can contact him at raphael@simpleseniorhealth.com.Simple Senior Health

{kind=link}

I loved this post, engaging and interesting to the reader. You have thought out the layers of content and the post is written for the reader and not pushed anything on them. Certainly gave me something to think about. Thanks for sharing.

Hey Raphael

What an awesome post! You almost lost me in the beginning, but once you put numbers to it, it all made perfect sense. Can’t believe I haven’t heard of the rule of 100 before.

I am already part of WA and have to second your opinion of it! It is the perfect way to start an online business with out all the flashy and often pushy upsells that so many of the other systems out there offer. A truly spam free, relaxed and helpful environment.

I actually joined iGrow before joining Wealthy Affiliate, The social network side of IT is an awesome idea in my opinion, but I lost interest in iGrow itself, because I did not have the knowledge to market it the way I would need to to make it pay off… Hence my finding WA.

Thanks for some valuable information. Keep up the awesome work!

Cheers,

Marc

Hello! I loved this post and found it very informative on how to supplement our income after retirement. A lot of people are facing this problem in their golden years while those should be the best. These are some great tips you suggest and everyone should read this. I have been using Wealthy affiliate for a few months now I absolutely love it. You can find some other hosts today but none offers the help that WA offers. Totally recommend this to everyone! Thank you for sharing!

That comment was so nice, it showed up twice! Hehe. Thank you, Katerina. I think of Wealthy Affiliate as a host/social network/educational system all rolled into one. You won’t lack for support here! Thank you so much for reading!

Hello Raph, thank you for bringing this wonderful post on how to supplement our fixed income with some other things that could be done via the internet to earn us money. I think I love the part of building a website, it is more solid and reliable.

I agree, Nnamdi! Thank you for responding. I built this website through Wealthy Affiliate and can say this, “My passions are out there for all to see.” I know I’ve helped a number of people through the website idea alone. The ability to gain income from it is just a plus.

Great post! Retirement is something we all think of but knowing the risk of investing is good to know also. I never did know what type I should go for so I always went safe (low risk) of course you do not get much out of that in the end lol.

Thank you Nichole. Depending on what kinds of funds you are willing to put towards an investment (or growth) vehicle, you can still get a decent return with low (or no) risk. Of course, full-on investing has the greatest potential for return, but also the greatest risk for loss. That rule of 100 is a great measure of when to do which. I hope this helps!

What a great article on making money when you are in retirement. I think a lot of people who are facing this stage of life are left wondering “what now”. Many people find themselves wanting to fill their time with something they love to do and have a passion about. Older people bring life experience into everything they do, including building their own business. I definitely thing this could be an advantage.

Thank you, Jean. It’s funny when I ask seniors, “So, what were you saving this money for?” and I get the puzzled response. A lot of people really have not thought about it. Maybe they’ve heard about a rollover, and know that they are supposed to do it, but don’t realize that there are lots of options depending on their goals. It is my goal to help bridge that gap and educate others.

Very well put together. I also like how you added in the graph. It looked like you also added the keyword to the title but added most a log with it. Seems like you got it figured out good job!

Thank you. I hope that people searching for these answers will find them through search engines. The more I reach, the better:)

Hey Raphael, this Wealthy Affiliate program seems pretty good. I have a question for you. If I sign up and get a free website, what happens if I don’t want to be a member anymore? Do I keep my website.

Thanks.

Thank you for responding, Nigel. As a starter, you do get two free websites. Of course, there is no cost to doing that. Wealthy Affiliate is providing the hosting, though. Since the site is on their server, it will stay on the internet. You won’t be able to edit the site without logging in there. It’s almost like having a site with a place like GoDaddy. You would still have to log into GoDaddy to edit it unless you moved it to a different host. My thought, though is that once you start, you won’t want to quit:)

Very well put thank you so much for your info this helps me a whole lot. You make it sound so easy . Adding you to fav bookmark

Thank you for reading Tiffaney. I’m pretty excited about IGrow in particular. It should be pretty awesome!